Institutional Insights: Goldman Sachs 'Weekend' Thoughts From The Trading Floor'

The quotation marks around “weekend” are intentional. Investors and traders haven’t had a real break in months, with “Green Dot Sunday” evolving from a one-off into a 2026 non-negotiable. The upcoming three-day “weekend” for U.S. markets is almost unwelcome: the holiday simply means another headline-driven session with zero price discovery and zero liquidity.

This weekend’s headlines remain highly fluid. This week, we faced two attempts at unilateral de-escalation, which resulted in even more supply. Thoughts and prayers to everyone impacted. Futures reopen in a few hours.

March began with a strong start and is ending on a similar note. Global fundamental managers are on track for their worst month since 2022, down 5.4% MTD, which pushes the cohort into negative territory for the year at -1.4% YTD. The numbers are even worse for fundamental U.S. Portfolios are down 5.7% MTD and 3.8% YTD. (h/t M. Laicini)

When you delve into the composition of the GS PB data, it becomes evident that investors are still trading as if they have a clear understanding of the market's direction:

Gross exposure hit a five-year high this week.

Net exposure has been reduced, but the composition is still being driven by risk-on flows—specifically short selling in both macro ETFs and single stocks.

Years ago, a client told me that when you’re truly panicked, you simply “get smaller”—you reduce both net and gross. That categorically has not happened in global books. Only net exposure has seen meaningful reduction. (h/t BT)

That’s the bad news.

The good news is that prices are finally starting to reflect the issues at hand, and the correction has at least begun. (NDX is now officially 10% off the highs.) It feels like we’re closer to the end than the beginning, but it also feels like we’re playing a game with no real innings in the classic sense—no one can give you a credible timeline. A lot of parties need to want de-escalation, and that still isn’t evident.

While it’s always tempting to be the sell-side strategist who claims to have called the bottom—and many have already tried—intellectual honesty suggests we’re simply not there yet.

A few things on my radar

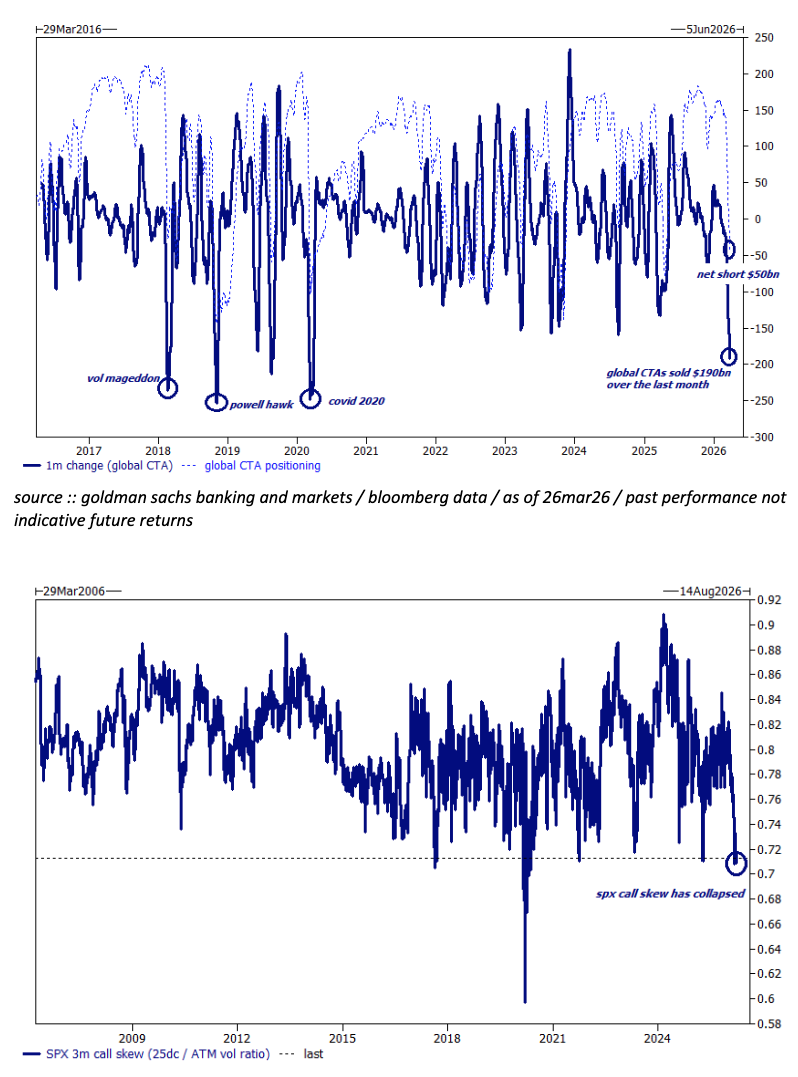

CTAs have sold even more global equities and are quickly approaching max short levels. At a minimum, that supply pressure is beginning to abate.

Main Street is finally noticing. Texts from college friends and family members are starting to show real panic: “BG, what did you do to the market?”

SPX call skew is collapsing. The market’s hope for a quick rebound is fading, which is showing up clearly in the cost of OTM upside strikes.

I’m scheduled to be out of office in exactly one week. History suggests we’ll finally get the Corr 1 event either right before I leave or while I’m away from screens.

Trades

Continue to like receiver trades / simply lower-yield expressions

Long EM equities that benefit from higher commodity prices

EWZ remains a favorite

Dom Wilson agrees

Short credit

still the only asset class that has yet to really flinch

SPX ratio call spreads

long the 2–3x structure

pitched last week, still like it, and adoption is building

Long gold

this trade is gaining followers

Good luck.

Across the Global Banking & Markets division

1) PB (i)

Hedge funds net sold U.S. equities for the sixth straight week, and at the fastest pace since April 2025. Our PB team sees early signs that capitulation may finally be starting to emerge.

2) PB (ii)

The global book was sold yet again and has now been net sold in 8 of the last 9 weeks. This marks the fourth consecutive week of short selling, driven by both macro hedges and single names. As above, these are still defensive but “risk-on” style flows.

3) One Delta

Trading remains effectively frozen, with a buyers’ strike on one side and ETF short management on the other. There are still no signs of real defense on weakness.

4) Futures (i)

Gold is down 15% MTD, driven by tighter financial conditions, renewed USD strength, lack of central bank support, and positioning. We think that may be enough. The core fundamental case for being long gold still holds, and any de-escalation could trigger a relief rally. (Cullen published charts yesterday and agrees.)

5) Futures (ii)

As noted above, CTA supply has been extreme, but at least it’s getting closer to exhaustion. The cohort has sold $190bn of global equities in the last month.

6) Derivs (i)

Despite how bad the last two sessions felt, SPX failed to realize what the weekly straddle had implied the preceding Friday. SPX gamma has been high and rich of late.

7) Derivs (ii)

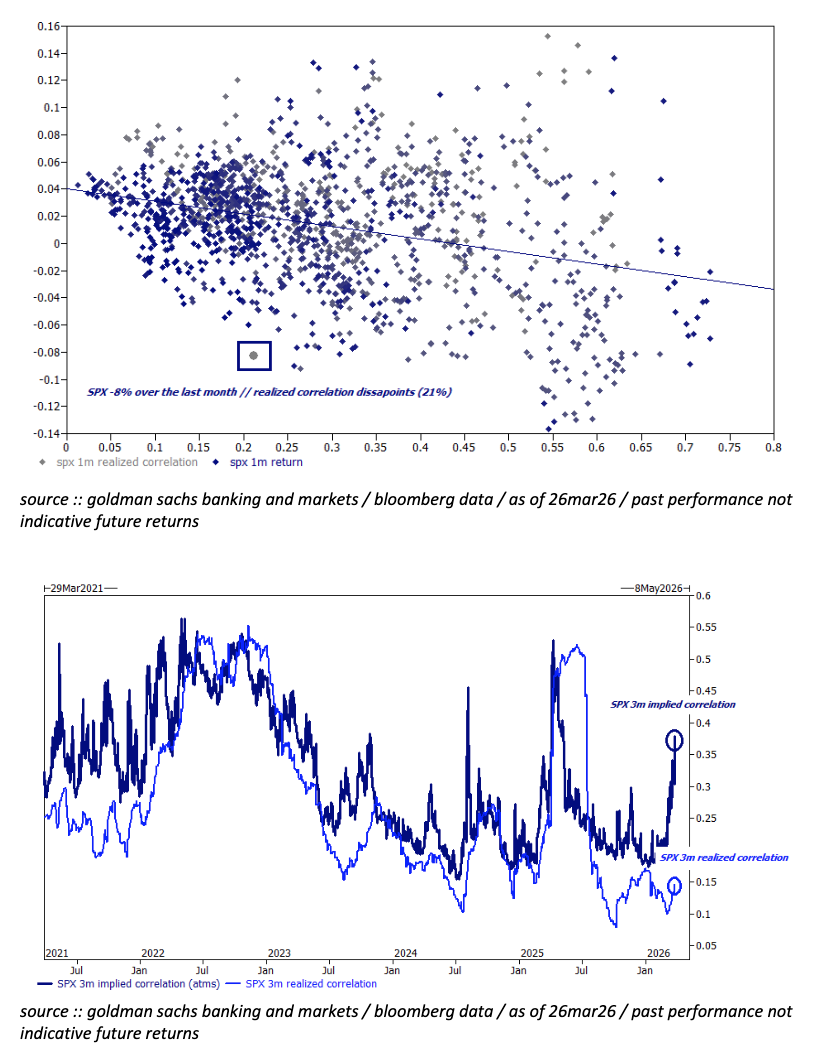

SPX realized correlation remains extremely low relative to the size of this drawdown. The desk continues to prefer sector ETF options or custom basket options for investors looking to express convexity views.

8) ETF Desk

ETFs have accounted for more than 40% of the consolidated tape on many sessions this month. When all else fails, trade the ETF wrapper.

Three highlights from the desk:

IXE / XLE is up for 14 straight weeks

+40% over that span

NDX / QQQ has traded lower for five straight weeks

U.S.-listed ETF AUM has grown for 37 consecutive months

now at $13.5tn

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!